1997 was the first year that global shipments broke the 100-MWp mark, and the US had a 42% share. After breaking the 100-MWp mark, manufacturers began pointing to the economies of scale that 100-MWp manufacturing capacity would bring. Back in the day, US solar cell and module manufacturing was primarily supported by oil or energy companies such as Arco, Shell, BP, and even Enron. The Walton family (think Walmart) was an early investor in CdTe manufacturer First Solar. Then and now, the US government, via DoE grants and loans, provides support for startup solar manufacturing but little support for ongoing commercial solar cell and module assembly manufacturing.

By 1999, driven by Japan’s strong residential rooftop incentive and government support, manufacturing shifted to Japan. Then, in 2007, boosted by the FiT-driven market and government manufacturing incentives, manufacturers in Europe, primarily Germany, took the lead.

Accelerating demand for PV installations in Europe – including the new multi-megawatt utility-scale application – strained the supply of polysilicon available to the PV industry. As a result, prices for polysilicon, wafers, cells, and modules increased significantly, increasing costs and margins for manufacturers and buyers.

In 2009, having built sufficient manufacturing capacity, China’s manufacturers entered the market with an aggressive pricing strategy that drove prices down by 42% in one year. Manufacturers in other countries could not compete with the low margins China’s manufacturers were willing to accept, and so – one after another – they failed.

Manufacturers in China were able to take advantage of government loans, grants, free or inexpensive land, low energy costs, and low labor costs to dominate global shipments from 2011 to the present day.

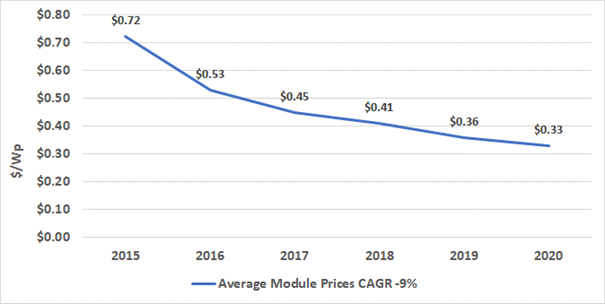

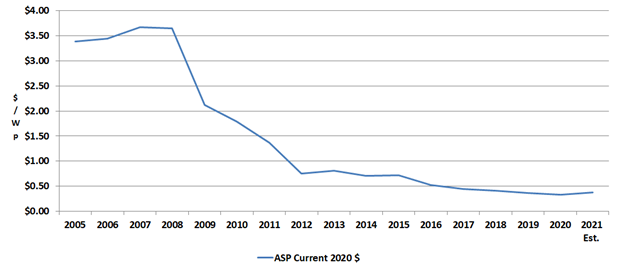

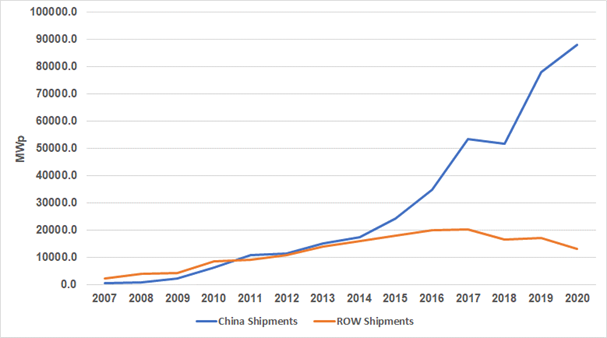

Figure 1 offers average module prices from 2005 through an estimate for 2021. Figure 2 presents shipments from China and the rest of the world from 2007 through 2020.

Figure 2 presents shipments from China and the rest of the world from 2007 through 2020.

Why do PV manufacturers fail?

In a perfect world, countries with demand for solar installations would have sufficient manufacturing to meet that demand. There are no perfect worlds. Buyers seek less expensive products. Meanwhile, manufacturing migrates to lower-cost areas with more manufacturing incentives. Governments, observing decreasing prices and assuming they represent progress, peg aid to further price decreases creating a landscape in which participants continue to chase goals that are, in reality, nothing but mirages.

Using the US as an example, dearly departed manufacturers include Siemens Solar, BP Solar, AstroPower, Evergreen Solar (ribbon), United Solar (a-Si), and the un-dearly departed Solyndra. Over the years, there were acquisitions (BP Solar and Solarex) and (ARCO, Siemens, and Shell Solar).

In 2004, eager to take advantage of the accelerating market for solar, GE acquired bankrupt AstroPower only to shut it down in 2009. Observing the success of CdTe manufacturer First Solar, GE acquired Colorado-based CdTe startup PrimeStar in 2011, announcing it would build a 400-MWp manufacturing facility. In 2013, having ramped nothing, GE sold PrimeStar’s technology to First Solar. China-based Hanergy acquired CIGS startups Global Solar and MiaSole.

Manufacturers fail for various reasons, so the best answer to – why do manufacturers fail? – is, it depends. However, solar manufacturers typically fail, and in some cases fail to launch, because of unrealistic expectations about cost and price and a lack of government patience and support. Companies that begin by chasing an unrealistic goal will never catch it.

The Prescription is Time and Money – Lots of Time, Lots of Money

As long as the metric for progress is based on an artificial cost curve, it will be difficult to build solar manufacturing capacity outside of China and Southeast Asia.

While offering demand-side incentives and a smattering of state-by-state manufacturing incentives, the US has chosen a stick approach, using tariffs on imports from China to protect, basically, no one. The US also, as indicated, provides grants and loans to startup manufacturing through the DoE. Currently, the country has one large thin-film manufacturer and several gigawatts of module assembly for crystalline. This year, Senator Jon Ossoff, Democrat, Georgia, introduced the Solar Energy Manufacturing Act and successfully negotiated to include it in the upcoming Congressional Budget Measure. It could pass as stands, be reduced in scope, or excluded from the final budget.

India has chosen a stick and carrot approach using high tariffs to discourage imports while introducing a production-linked incentive to encourage manufacturing to locate in the country. India will need to keep its incentive in place long enough to support its new manufacturing base against competitively priced imports.

Across Europe, no stick and a smattering of manufacturing incentives has done little to encourage domestic supply. The EU might consider a production incentive similar to India that stays in place long enough to support a fledgling industry. A Buy-European incentive would help to encourage domestic buying.

Countries looking to start up photovoltaic manufacturing will need patience and the willingness to support the effort for years. Though carrot and stick approaches are common, manufacturers usually pass the tariffs on to buyers, increasing cost. Maybe it’s time for a two-carrot approach – incentives for buying domestically produced cells and modules along with manufacturing incentives.

The solar industry has gotten a bad rap for always having its hand out. The conventional energy industry has had its hand out for decades. To build a domestic supply chain, governments might consider offering solar manufacturers the same embedded incentives available to oil, coal, and natural gas, incentives embedded in the energy structure to the degree that they become invisible to the public over time.