Since 2015 average module prices reliably decreased – year, after year – convincing buyers, and the industry as a whole, that an increase not just unlikely but impossible.

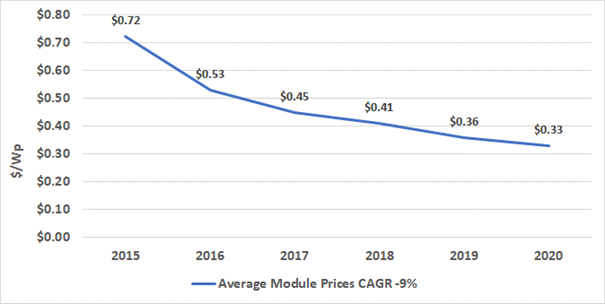

From 2015 through 2020, average module prices decreased by a compound average of 9%. Figure 1 presents average module prices from 2015 through 2020.

Figure 1: Average Module Prices 2015 through 2020

Manufacturing in the solar industry has been low margin for decades, yet average prices either decreased or remained flat for over ten years. Manufacturers in China and Southeast Asia seemed to accept low margins, thus creating an uncompetitive landscape for manufacturers in other regions and countries.

In 2021, buyers find themselves faced with module price increases. The current pricing situation has some aspects in common with the mid-2000s. During these years, Germany’s Feed-in-Tariff law encouraged demand in the country to accelerate. Other countries in Europe rapidly followed suit, creating, almost overnight, a gigawatt level market for solar deployment.

The feed-in tariffs were intended to drive demand – and they worked even better than envisioned. Though proponents expected accelerated demand, sufficient thought was not given to how the speed of market acceleration would impact upstream participants such as polysilicon suppliers.

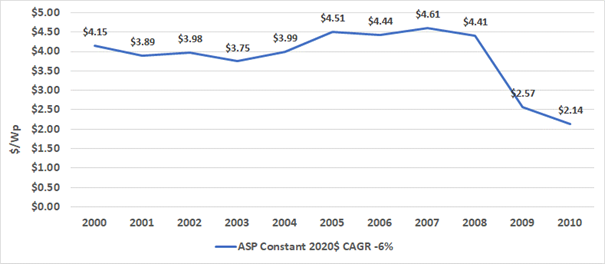

Previous to the FiT, the photovoltaic industry had primarily survived on scrap. The polysilicon industry’s largest customer was the semiconductor industry. Feed-in-tariffs marked the end of this paradigm and beginning in 2004, polysilicon prices spiked, rising in some cases to $400/kilogram on the spot market with contracts spiking almost overnight from $20 to $30/kilogram to >$60/kilogram. Wafer, cell, and module prices also increased with buyers captive to the increase. Polysilicon, ingot, wafer, and cell producers funded capacity growth via long-term contracts. New cell and module manufacturers sprang up almost overnight, each believing that prices would not decrease. Then, in 2009 PV manufacturers in China had sufficient capacity to enter and, using aggressive pricing strategies, rapidly drove manufacturers in other countries out of business.

Figure 2 presents average module prices from 2000 through 2010.

Figure 2: Average Module Prices 2000 through 2010

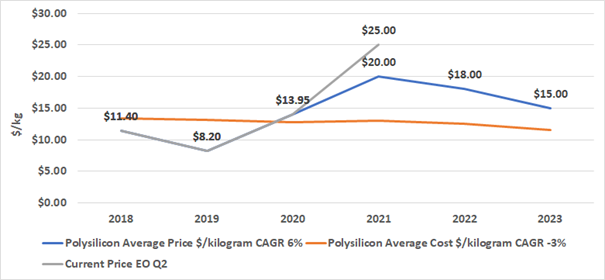

As with the earlier period, demand for solar is accelerating, driving a need for more polysilicon. Unfortunately, in 2020 accidents in several facilities in China took significant capacity off-line. Repairs took time because of the pandemic and because, well, repairs take time.

Glass supplies were also impacted. Due to overcapacity, China’s government has controlled glass supply for years, allowing additional capacity, only replacement capacity. As the demand for bifacial modules accelerated, the available supply of solar glass was unable to keep up, and prices rose. Mid-2021, glass supply constraints have eased, but prices have stayed high.

China has also been experiencing a coal shortage, which has driven the price of energy up in the country. Much of China’s solar production is powered by coal, and the shortage has led to higher energy prices for manufactures from polysilicon downstream to modules.

Back to polysilicon, capacity additions take over a year. Though additional capacity is planned and being constructed, it will not come online rapidly nor – for the sake of quality – should it. And, as wafer and cell manufacturers are adding n-type capacity, a higher grade of polysilicon is required.

Also, 45% of China’s polysilicon capacity is in Xinjiang. The US has banned materials from Xinjiang and will see supply constraints. If other countries and regions take similar actions, the industry would see a down year in shipments and construction activity. Finally, China’s manufacturers may have discovered that healthy margins are a good thing and may be unwilling to offer premium products at low margins in the future.

Figure 3 offers average polysilicon costs and prices from 2018 through 2023, along with the current price.

Figure 3: Polysilicon Prices 2018 through 2023

Module pricing is likely to be volatile in 2021, with potential spikes and little relief for buyers. As prices for wood, steel, and aluminum are also high, there is high potential for construction delays, with some developers choosing to wait out the situation.

Buyers should be aware that prices may not decrease for some time – then again, all it takes is for one multi-gigawatt manufacturer to break ranks and drop prices. It’s a pricing game of chicken. Developers worldwide can only delay projects so long while manufacturers concentrated in China and Southeast Asia hold all of the supply cards.

Figure 4 presents average module prices.

Figure 4: Average Module Prices