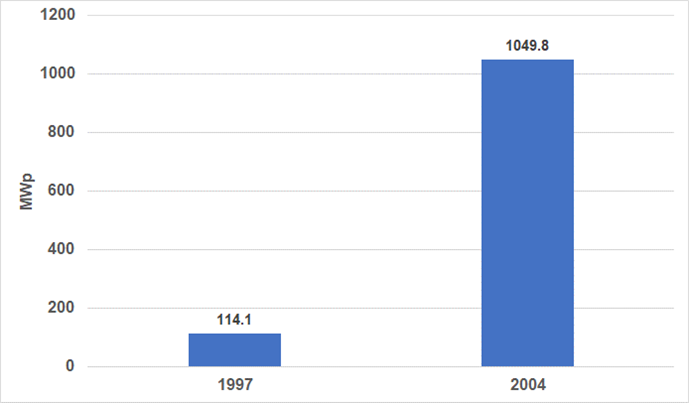

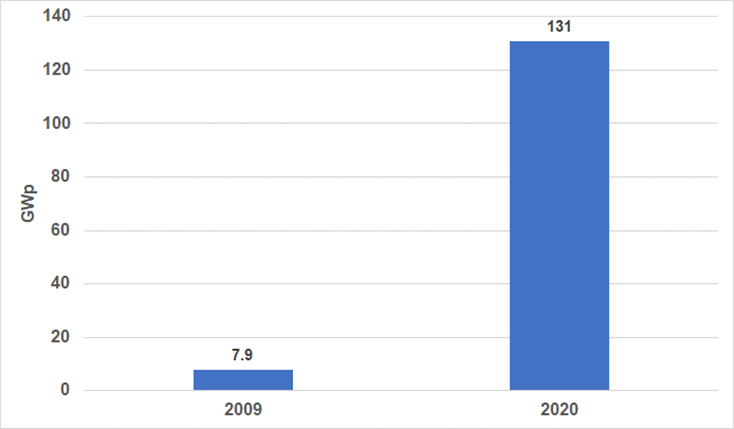

Shipment Progress 1997, 2004, 2009, 2020

1997 was the first year shipments topped 100 MWp and manufacturers looked to 100-MWp of capacity to provide economies of scale

In 2004, the industry topped 1-GWp in shipments and manufacturers pointed to 1-GWp of capacity as the economies of scale benchmark

In the mid-2000s, manufacturers in Taiwan and Europe planned to become pure play cell manufacturers

In 2009, with shipments nearing 10-GWp annually, manufacturers focused on 10-GWp of capacity to provide economies. Pure play cell manufacturing fell out of favor.

After 2020 – capacities of >30-GWp are the focus and pure play cell manufacturing is back!

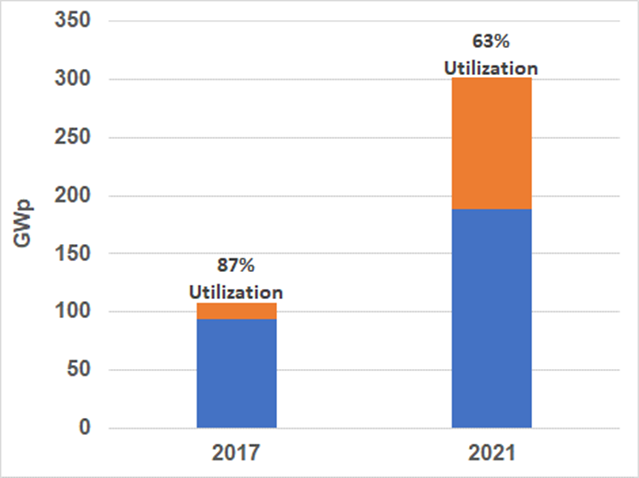

Economies of Scale – the good, the bad, and the underutilized 1987, 2007, 2017, & 2021 Estimate

Unused capacity is a cost to manufacturers.

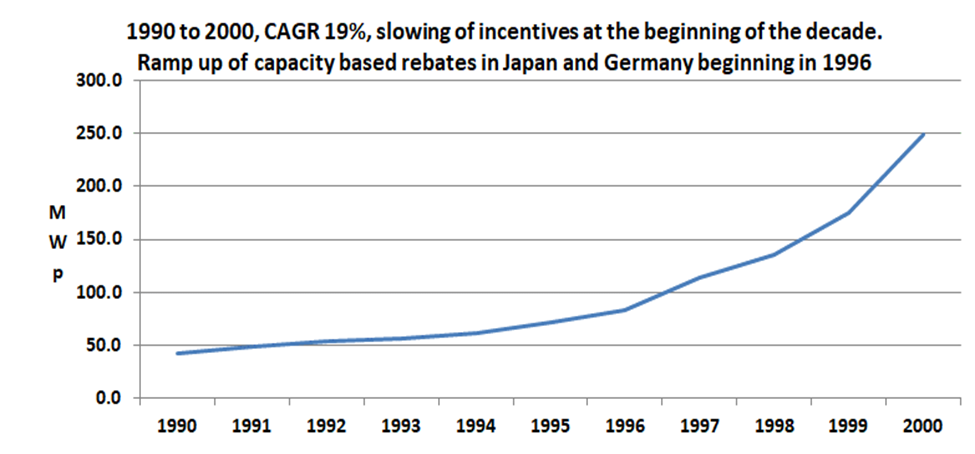

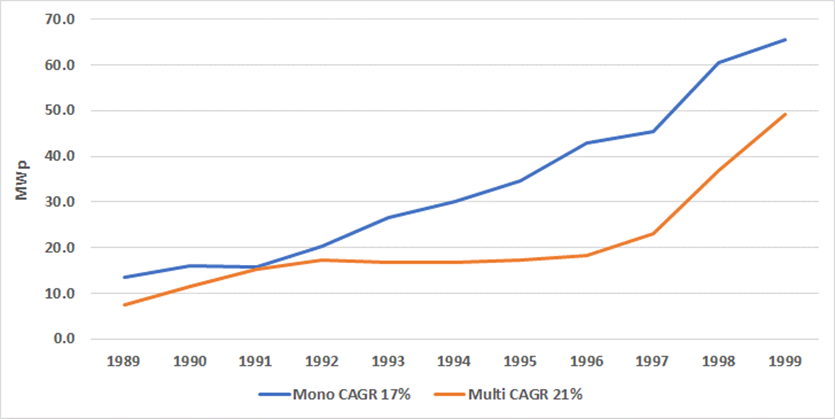

Shipments 1989 through 1999, all Technologies

In the early days of the PV industry, shipments of standard monocrystalline technology dominated. In the 1980s into the early 1990s, amorphous silicon performed well, losing share when the consumer-indoor application (watches, calculators) declined, and it failed to prove less expensive to manufacture.

Crystalline Shipments 1989 through 2009

In 1998, multicrystalline, which was less expensive to manufacture, began gaining share in the market.

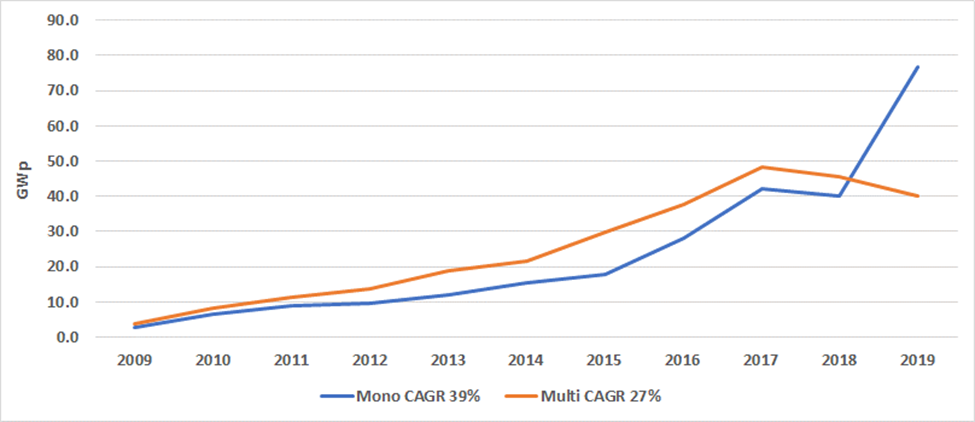

Multicrystalline took the major share of shipments in 2003. At the same time, shipments from China began taking share from manufacturers in Europe, Japan, and the US.

Crystalline Shipments 2009 through 2019

Though it seems to be an overnight shift from multi to monocrystalline, the change began much earlier. In 2012, manufacturers began adding p-type mono and multicrystalline PERC capacity, primarily focusing on p-type mono-PERC.

In 2018, manufacturers began shipping significant volumes of PERC, particularly monocrystalline.

A little Pricing History …

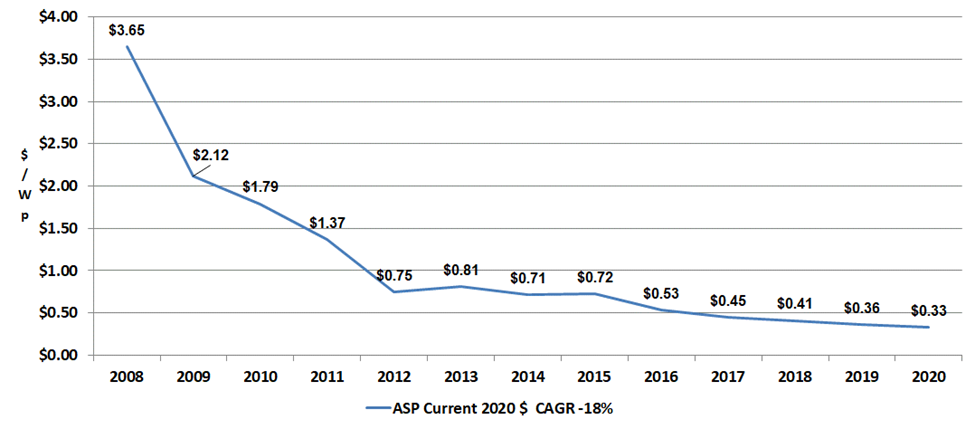

Since 2009 the accurate cost of PV cell and module manufacturing has been obscured by subsidies. Price is a market function and not a reliable indicator of manufacturing progress. Module prices are currently increasing.

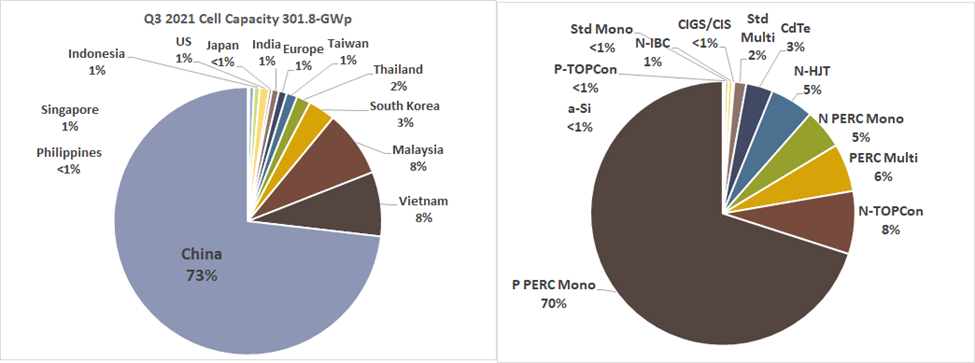

Current Industry Cell Capacity

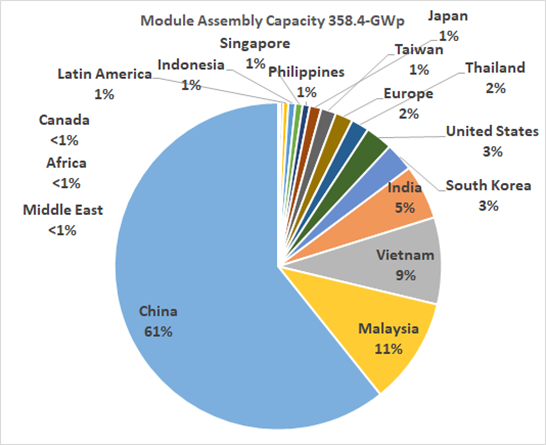

Current Module Assembly Capacity

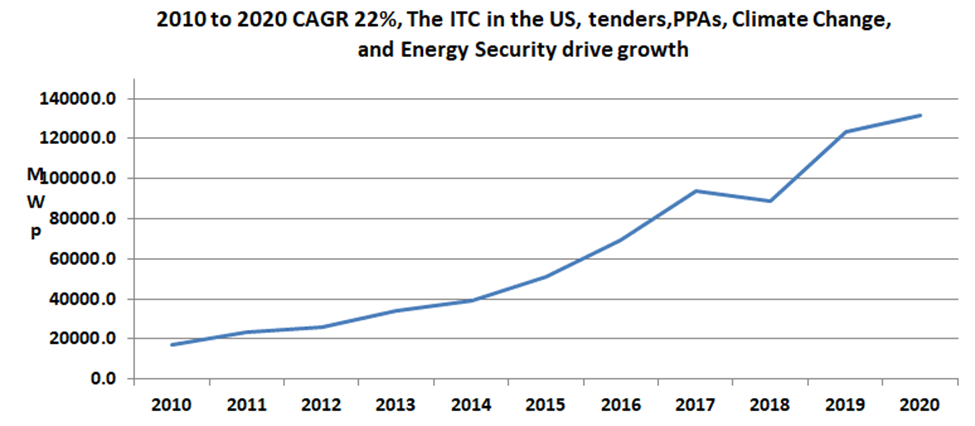

Shipments 2011 to 2021 estimate

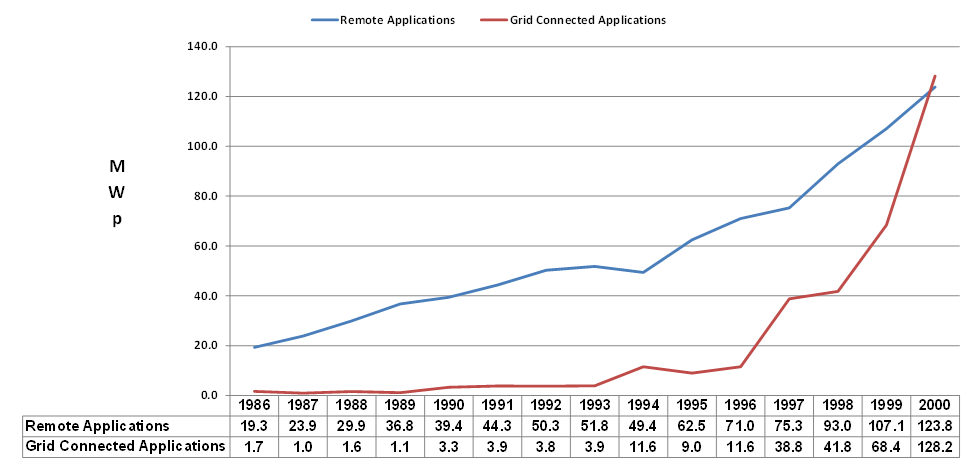

Once upon a time off-grid dominated

Off-grid (remote) solar deployment uses storage – in the past, lead acid batteries. Progress with storage has been slower than hoped as it was thought of as too expensive. Now, the future depends on it.

To truly become one of the industries of the future solar needs to:

1. Have a supply chain free of forced labor.

~45% of polysilicon is produced in Xinjiang

Metallurgical Silicon producer Hoshine serves clients outside of China

~60% of cobalt is manufactured in the Congo

2. Have a supply chain free of conventional energy.

Much of the world’s metallurgical silicon, polysilicon, wafers, cells, and modules are produced using coal as an energy source.

3. NOT provide electricity to coal and other dirty mining enterprises.

Solar installations are commonly used to provide electricity for mining – including coal

4. Have manufacturing in ALL countries with solar demand.

The industry provides jobs in science, engineering, manufacturing, and construction – jobs, jobs, jobs

5. Have a diversified workforce.

6. Be transparent about ALL the cost components of PV manufacturing – meaning ALL incentives, grants, loans, debt – everything from consumables to polysilicon to glass, aluminum, et al, so that the industry has a clear cost curve with which to track progress.

7. Accept that manufacturers need more than a 5%, 10%, 15% margin to run operations.

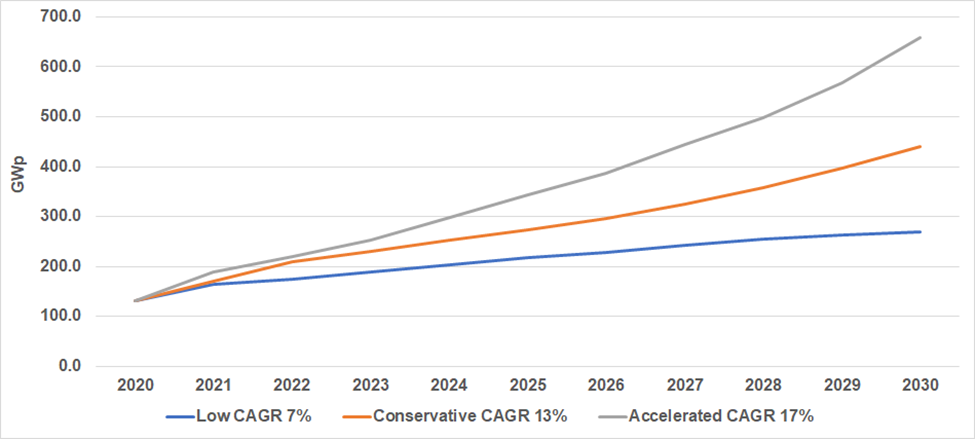

Forecast

The accelerated and conservative forecasts need a global manufacturing effort to come to pass and there must be sufficient capacity for all materials.

For storage to play a significant role, battery technologies need continued research effort – including into cobalt free battery technologies – and storage must play a significant role in a modernized grid.

“There are only two ways to live your life. One is as though nothing is a miracle. he other is as though everything is a miracle.” Albert Einstein